The Q2 numbers are out regarding lower middle-market transactions, and the data, as well as our experience during this time point to the same fascinating and counterintuitive set of dynamics in the marketplace that we believe will persist for the remainder of 2020. In short, there are two feelings that appear to be omnipresent but misguided: 1) among sellers, there is the feeling that now is a bad time to sell; and 2) among buyers, there is a feeling that they are missing good deals, or that bargains are to be had.

We will explain current market dynamics to demonstrate that, at least presently, those feelings generally are not translating into reality. We will show that right now is one of the best times to sell for pandemic-resistant businesses, particularly in light of the extended valuation recovery periods for previous recessions.

Seller Sentiment

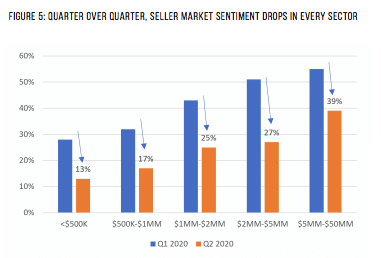

As we attempt to define what reality is, let’s start with what sellers are feeling. It’s not good. According to the International Business Brokers Association (IBBA) Q2 2020 Market Pulse report, “Seller market sentiment dropped to record lows this quarter, falling well below levels seen during the last eight years.”

Practically, what does this mean? It means sellers are generally not feeling good about the present being a good time to sell. This makes sense, right? People are still feeling very uncertain about the future. According to a recent Washington Post article, a Gallup survey in mid-July showed 73 percent of adults viewed the pandemic as growing worse — the highest level of pessimism recorded since Gallup began tracking that assessment in early April. Another Gallup Poll, published Aug. 4, found only 13 percent of adults are satisfied with the way things are going overall in the country, the lowest in nine years. Widespread “brain fog” has been reported, which psychologists have indicated is likely due to chronic stress and anxiety associated with the pandemic. In short, the country is in a bit of a mental crisis, and business owners are not immune to it.

One other factor that may be leading to Sellers’ concerns about selling now are PPP Loans. According to Andy Kocemba, President & CEO of Calhoun Companies, “Owners are confused about the ability for the loan to carry over to a new owner, so they’re choosing to wait to sell rather than risk having to pay back the loan.” (Note: PPP Loans are transferable if done correctly).

What has been the result of Sellers’ reluctance to sell presently? According to Scott Bushkie, Managing Partner, Cornerstone Business Services, “We’ve talked with multiple private equity firms, and they’re estimating the flow of potential new deals coming their way is down 50-70% over 2019.” In short, sellers have pulled back from going to market. Interestingly, this is consistent with Great Recession behavior where sellers, focusing on their businesses, believing most buyers to be bottomfeeders, and not wishing to take a hit on valuation pulled back, causing latent supply to build for years.

In short, the feeling is that it’s not a good time to sell. But is that a fact? Let’s look at buyer activity.

Buyer Sentiment

According to BizBuySell.com’s Q2 2020 Insight Report, over the same period (April-June 2020) that small business transactions dropped 39%, “the number of buyers searching and inquiring about businesses on BizBuySell recovered then eclipsed pre-pandemic levels.”

Who are these buyers? It’s very interesting. Just as in 2009-2010, many buyers are newly unemployed, 28% presently. Other buyers are business owners themselves, looking to expand their footprint or add products and services through vertical integration. And lastly, according to Kyle Griffith, Managing Partner of The NYBB Group, “In the $5 million and up sector, private equity made five-times the acquisitions over existing companies in Q2. That’s a significant presence and one we haven’t seen to such an extent in the past.” In short, buyer demand is surging, which is consistent with what happened during the Great Recession.

Our general sense is that many buyers are frustrated. At Calder, we are receiving a barrage of inquiries from family offices and private equity firms searching for business opportunities. It is important to remember that these investment firms often have significant capital and mandates to deploy it. Just because a pandemic hits doesn’t mean that a core reason for their existence evaporates.

Additionally, we are receiving dozens of inquiries per week from individual buyers who have been spurred into entrepreneurship due to employment shakeups and/or a general disdain for wanting to remain in the corporate world.

Business Valuations Are Holding Up!

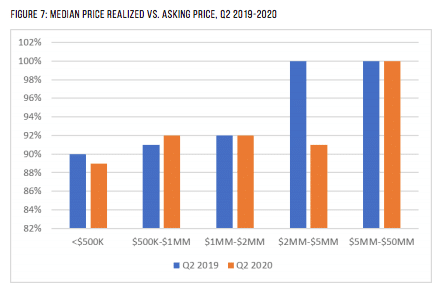

Business valuations are holding up very nicely. Fundamentally strong businesses are experiencing buyer competition, and quality deals are receiving full prices. According to IBBA data, “in Q2, median final selling prices came in anywhere from 89% to 100% of pre-set asking price or internal benchmark. Lower middle market companies in the $5 million to $50 million range achieved the highest values at 100% of benchmark.”

According to BizBuySell data, the median sale price of businesses sold in Q2 rose 6.1% compared to 2019. According to the report, “This point may serve as a rude awakening for the 58% of surveyed buyers looking for a business…while expecting a favorable price.”

According to the report, “If your goal is to buy a business that has been profitable during the pandemic, you’re going to pay a premium for the reduced risk.”

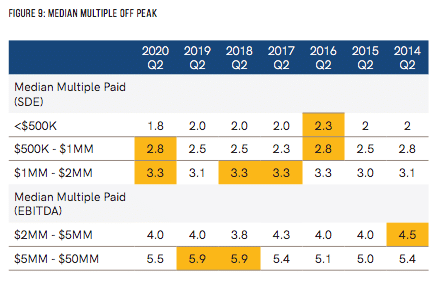

Current & Historic Multiples Based on Business Size:

Deal Structure is Still Solid

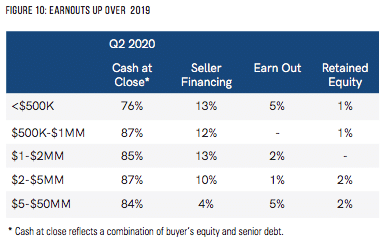

Here is a snapshot of reported deal structure based on size of business over the past quarter:

“Frankly, I think we expected a bigger jump in seller financing…” stated Lisa Riley, Principal at Delta Business Advisors.

Our Experience At Calder

Our experience has been very similar to the broader market, which is why we want to get our bullhorn out and shout. Sellers have been very reluctant to move forward because most are feeling like now is not a great time to sell due to the pandemic. However, those sellers whose businesses have held up well and have decided to go to market have experienced intense buyer interest, multiple offers, and accepted letters of intent (LOI) at or above the original benchmarked valuation.

Here is a timeline of how things have transpired for a number of our engagements:

| Type | To Market | Under LOI |

| Woodworking Manufacturer | June 2020 | July 2020 |

| Construction Services Company | April 2020 | July 2020 |

| Millwork Manufacturer | March 2020 | July 2020 |

| Industrial Services Company | June 2020 | August 2020 |

| Project Management Company | April 2020 | July 2020 |

| Cellulose Insulation Company | May 2020 | July 2020 |

In summary, for businesses that have demonstrated strength, now is an excellent time to sell for the following reasons: buyer demand exceeds pre-pandemic levels leading often to competitive offers, valuation multiples are holding up, cash at closing is remaining strong, and most buyers are not actively seeking distressed businesses.

Looking Forward Using the Past

We have no way of knowing how long the existing market dynamics favorable to sellers will last. There are already factors that are pushing against us, and these factors will likely increase in prevalence before receding. For example, going forward:

| Deal Structure | Likely to see increased sale proceeds in the form of earnouts and/or rollover equity. |

| Due Diligence | Due diligence is likely to require increased timeframes as buyers seek to assess the current and future impact of COVID. |

| Lending Environment | Recent tightening of credit markets may result in more buyer self-financed transactions and/or greater seller financing. |

One final item that should cause sellers to consider their exit timeframe. According to Thomson Reuters, following the dot-com bubble and recession, valuations declined 22% from peak to trough, and it took 7 years for valuations to rebound to pre-recession levels (1997-2004). Similarly, valuations declined 27% during the Great Recession, and it again took 7 years (2007-2014) for valuations to rebound. Given these truths from the past, it is entirely feasible that over the coming years, valuations may decline 20-30% and that it may take many years for levels to recover to pre-pandemic levels.

To conclude, it’s critical to assess the facts of the marketplace before drawing definitive conclusions about how things are. Feelings are not facts and that may be particularly true during this time of unprecedented mental malaise.

We continue to be confident. Just as they did during the early 2000s and through the Great Recession, deals will get done, and American entrepreneurship and grit will persevere. According to Calder Managing Partner, Max Friar, “We’re up to 20 closings already in 2020, 3.5 months ahead of 2019. Our goal is to spread the message to quality sellers that now may be an excellent time to exit. We look forward to continuing to break our own records!”

If you are interested in buying or selling a business, please contact Calder confidentially.

Sources: